When planning your estate, two taxes often come into focus: Capital Gains Tax (CGT) and Inheritance Tax (IHT).

Although they are sometimes confused, they apply in very different circumstances.

Understanding how these taxes work can help you make informed decisions, protect your family’s wealth and potentially reduce future tax liabilities through careful planning.

Whether your estate includes property, investments or a family business, knowing the rules today can make a significant difference for the next generation.

What Happens to Capital Gains Tax When Someone Dies?

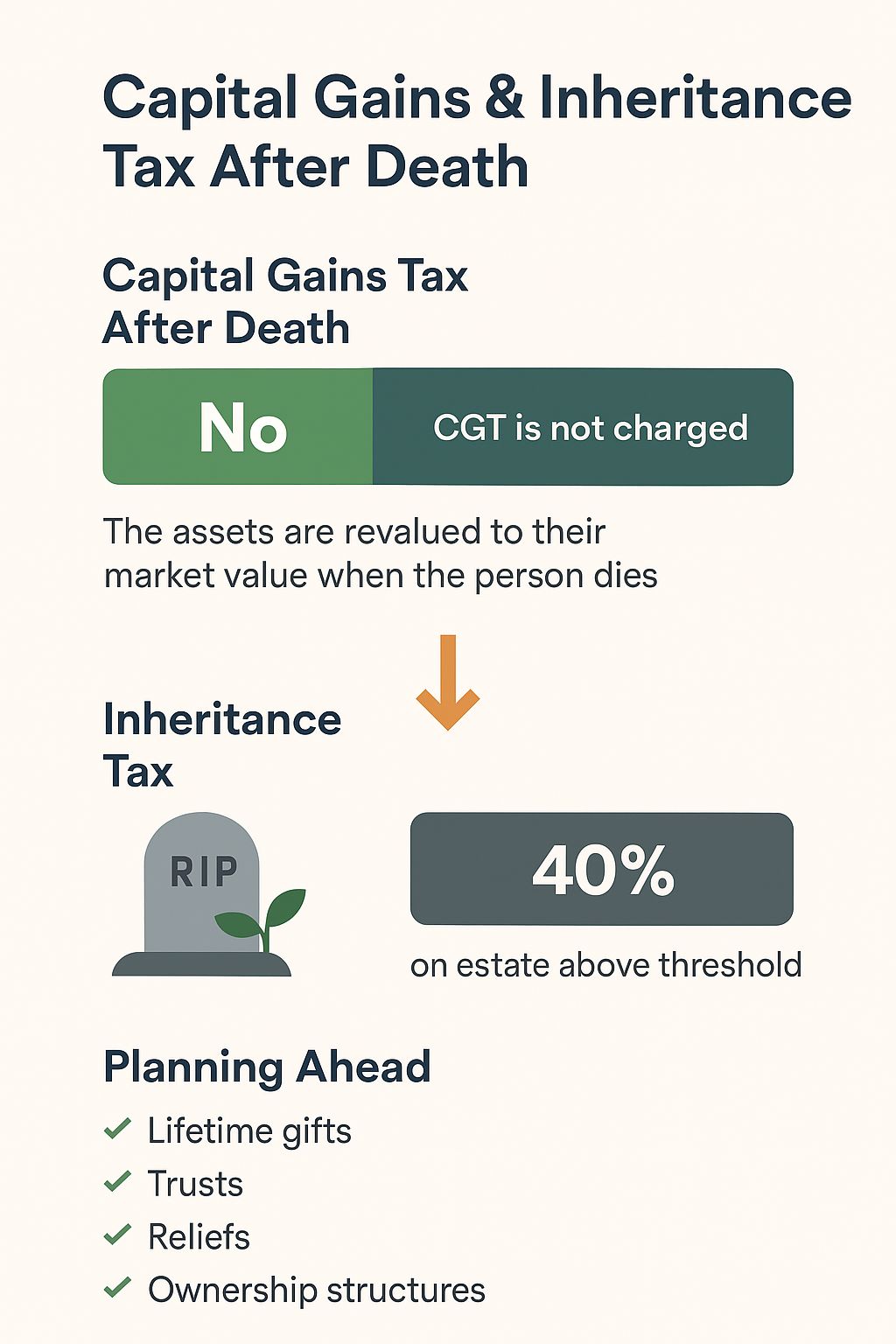

One of the most common misconceptions is that Capital Gains Tax becomes payable when someone dies.

In most cases, this is not the case.

When an individual dies, Capital Gains Tax is not charged on the increase in value of their assets at that time.

Instead, the assets generally receive a market value uplift.

This means that beneficiaries inherit the assets at their market value on the date of death, and that value normally becomes the starting point (or base cost) for calculating any future Capital Gains Tax if the asset is later sold.

Example

Imagine you purchased a property for £100,000.

By the time of your death, it is worth £300,000.

The £200,000 increase in value is not subject to Capital Gains Tax on death.

If your beneficiary later sells the property, any Capital Gains Tax will usually be calculated using £300,000 as the acquisition value, rather than the original purchase price.

What Is Inheritance Tax?

Inheritance Tax is a tax charged on a person’s estate after they die.

An estate includes assets such as:

- Property.

- Savings.

- Investments.

- Business interests.

- Personal possessions.

The amount of Inheritance Tax payable depends on the value of the estate and the reliefs available.

Current Inheritance Tax Allowances

For many estates, the following allowances may apply:

- £325,000 Nil Rate Band (NRB).

- Up to £175,000 Residence Nil Rate Band (RNRB) where the qualifying conditions are met and the family home is left to direct descendants.

Any value above the available allowances may be subject to Inheritance Tax at 40%, unless an exemption or relief applies.

When Is Inheritance Tax Not Payable?

Inheritance Tax may not apply, or may be reduced, in several situations.

Common examples include:

- Assets left to a spouse or civil partner.

- Gifts to qualifying charities.

- Certain qualifying business assets.

- Certain qualifying agricultural assets.

- Estates that fall within the available tax-free allowances.

Every estate is different, so professional advice is important before relying on any relief.

How Estate Planning Can Reduce Future Tax Liabilities

Effective estate planning is about more than reducing tax—it also helps ensure your wishes are carried out and your assets are passed on efficiently.

Depending on your circumstances, planning may include:

- Making lifetime gifts.

- Using trusts where appropriate.

- Reviewing ownership of assets.

- Considering Business Property Relief where available.

- Considering Agricultural Property Relief where available.

- Reviewing wills and succession plans.

Starting early often provides more planning opportunities than leaving decisions until later in life.

Why Planning Early Matters

Many families only begin thinking about estate planning after a major life event.

However, early planning can provide:

- Greater flexibility.

- More tax planning opportunities.

- Better protection for family wealth.

- Clear succession arrangements.

- Peace of mind for future generations.

Estate planning is not only for high-net-worth individuals—many homeowners and business owners could benefit from reviewing their affairs.

How Business Management Consultation Can Help

At Business Management Consultation, we provide practical advice tailored to your family’s circumstances.

Our services include:

- Inheritance Tax planning.

- Capital Gains Tax advice.

- Estate planning strategies.

- Business succession planning.

- Business Property Relief guidance.

- Tax-efficient ownership structures.

- Family wealth planning.

- Ongoing tax advice.

We work with individuals, families and business owners to help preserve wealth while ensuring compliance with UK tax legislation.

Conclusion

Although Capital Gains Tax is generally not payable on death, Inheritance Tax may still apply depending on the value of the estate and the reliefs available.

Understanding the difference between these two taxes is essential when planning how your wealth will pass to future generations.

By reviewing your affairs early and seeking professional advice, you may be able to reduce unnecessary tax liabilities and ensure more of your hard-earned wealth benefits the people you care about most.

If you would like tailored advice on estate planning, Inheritance Tax or Capital Gains Tax, we’re here to help.

Call us today on 01273 777 333 to arrange your free consultation.

Leave a comment