As businesses expand across borders, it becomes increasingly common for companies within the same group to buy and sell goods, provide services or make loans to one another.

While these transactions may seem straightforward, HMRC has strict rules to ensure they are carried out on a fair commercial basis.

These rules are known as transfer pricing.

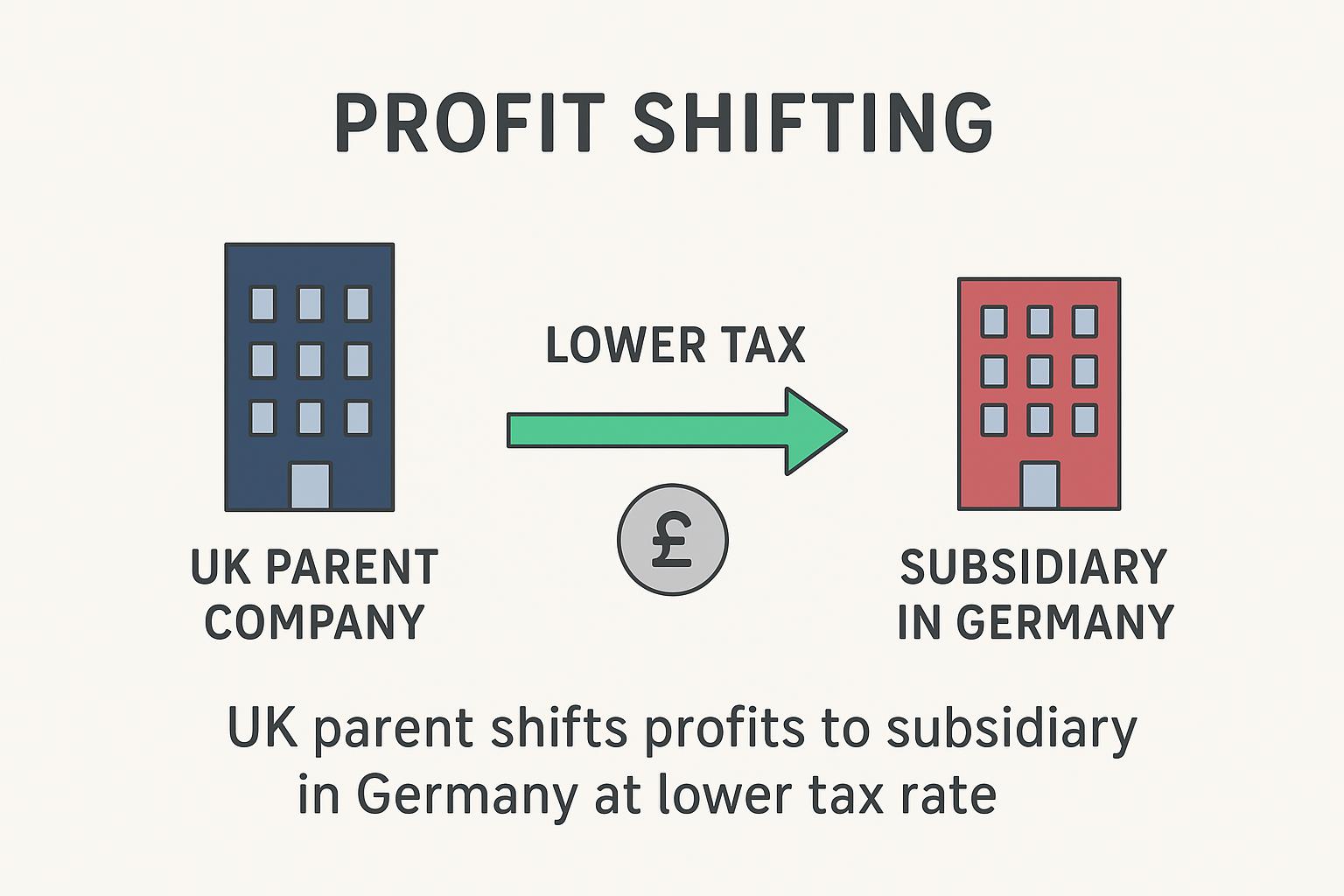

Transfer pricing is designed to prevent profits from being artificially shifted between countries and to ensure businesses pay the correct amount of tax where economic activity takes place.

If your business operates internationally, understanding these rules is essential.

What Is Transfer Pricing?

Transfer pricing refers to the prices charged between connected or associated companies in different countries.

Examples include:

- Selling goods between group companies.

- Charging management or consultancy fees.

- Licensing intellectual property.

- Charging interest on loans.

- Providing shared services.

- Selling or transferring business assets.

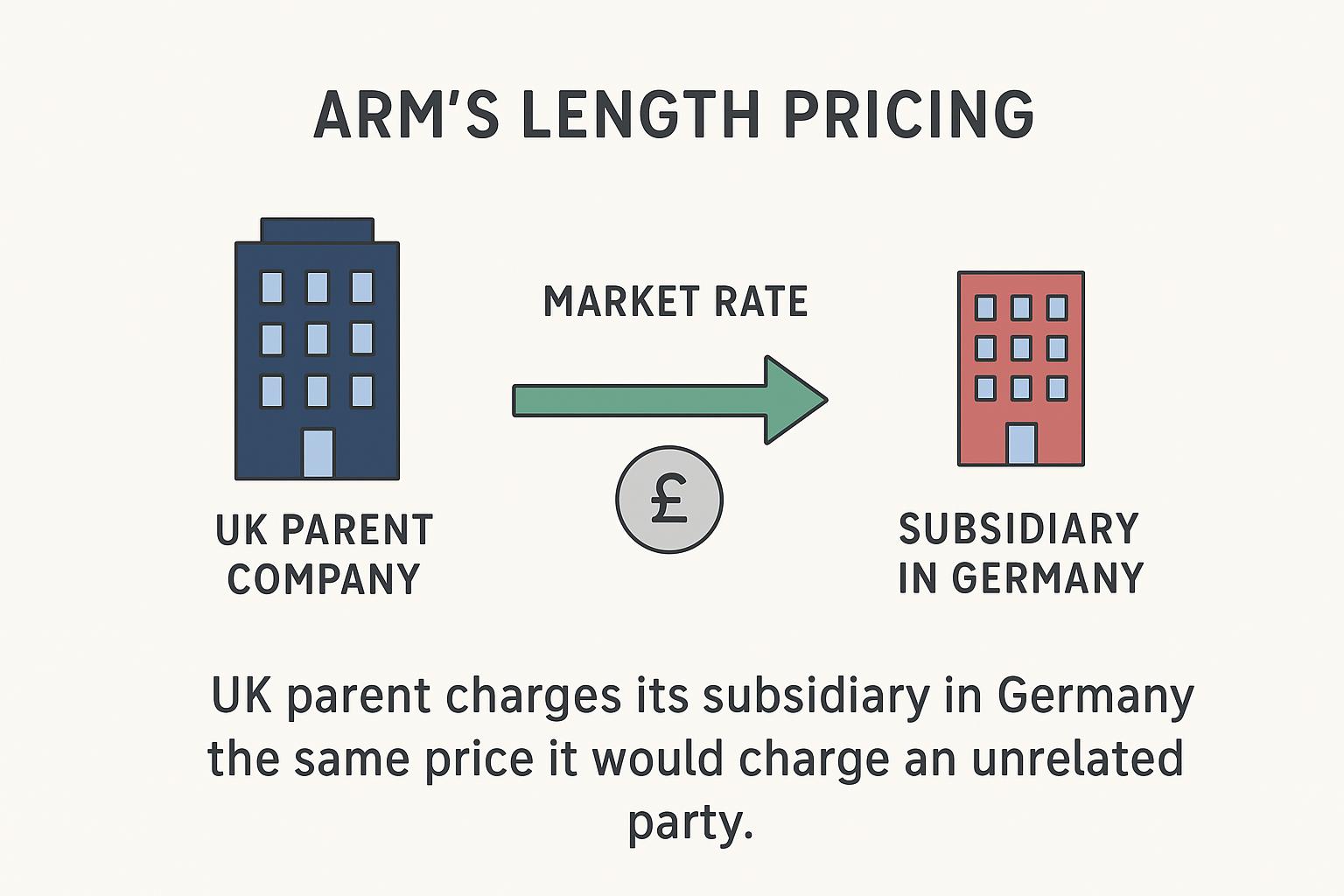

HMRC expects these transactions to follow the Arm’s Length Principle, meaning the prices should be the same as those that would have been agreed between independent businesses dealing under comparable circumstances.

Why Does Transfer Pricing Matter?

Transfer pricing rules exist to ensure that profits are reported and taxed in the appropriate jurisdiction.

They help to:

- Prevent artificial profit shifting.

- Promote fair taxation between countries.

- Reduce the risk of tax avoidance.

- Support international tax transparency.

- Provide greater certainty for multinational businesses.

Failure to comply can lead to enquiries, tax adjustments, interest charges and, in some cases, penalties.

Leave a comment